Ninety-two per cent sold on day one. S$1,893 per square foot. And the government still calls it affordable housing. The Executive Condominium market just had its most revealing moment at Rivelle Tampines, and most buyers walked past the warning sign with a cheque in hand.

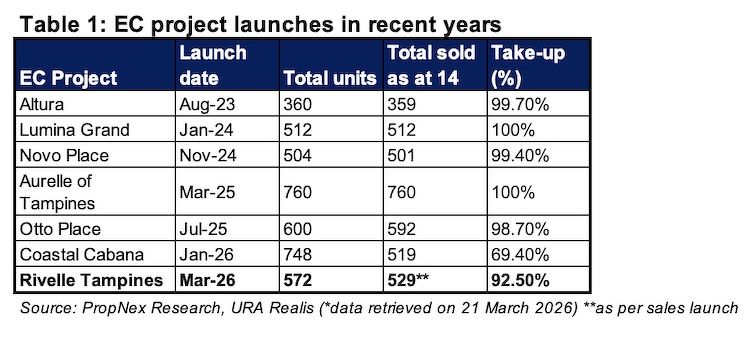

On 21 March 2026, 529 out of 572 units at Rivelle Tampines Executive condominium were sold in a single weekend, at an average price of S$1,893 psf. I was watching the queue that day. These were not struggling young couples scraping together a first home. Many were upgraders with strong savings who had clearly done this before. This is not a middle-class housing scheme anymore. It is a wealth-building game for people who are already doing well.

Is the Executive Condominium Singapore Still for the Average Family?

The original idea behind the Executive Condominium was simple. You get a private condo feel at a 20 to 30 per cent discount, plus a CPF grant of up to S$30,000 for first-time buyers. That sounded fair a decade ago. It does not hold up today.

According to a Business Times analysis published on March 31, 2026, a three-bedroom EC at 900 square feet priced at S$1,900 psf costs S$1.71 million. For a household earning the maximum allowed income of S$16,000 a month, that works out to 8.9 times their yearly pay. Financial experts consider anything above 5 times to be stretched. At 8.9 times, you are not buying a home. You are making a bet.

The same BT report notes you need S$427,500 in cash and CPF savings just to cover the downpayment, based on the 75 per cent loan limit. If your savings are not already large, you are not really in this market. You are watching others build wealth with a government subsidy you helped fund.

Pay Now or Pay Later: The Risk Hidden Inside the Deferred Payment Scheme

Here is the number that should be in every headline. According to the Business Times, an estimated 71 per cent of buyers at Rivelle Tampines chose the Deferred Payment Scheme, known as DPS. Under DPS, you pay 20 per cent upfront and nothing more until the building is ready, which at Rivelle Tampines will be around 2030. It sounds flexible. In many cases it is a financial trap.

Here is why. When you use DPS, you skip monthly loan payments for three to four years. That also means you skip the real-world test of whether you can actually afford the loan. In 2030, when the keys are ready, the bank runs that test properly. If your income has dropped, or interest rates have gone up, the bank may say no. The developer can then cancel your purchase and keep your 20 per cent deposit. On a S$1.74 million unit, that is S$348,000 lost.

The BT report points out that standard private condos in Singapore are not allowed to offer DPS. An EC comes with a government land subsidy, so it should have stricter rules, not looser ones. The 30 per cent mortgage servicing cap from MAS is designed to protect buyers from overcommitting. DPS lets you sidestep that pressure at signing. It does not make the pressure go away. It just delays it by four years. (The full article is available to Business Times subscribers.)

Three Changes That Would Actually Fix This

The Business Times piece makes three clear recommendations. I agree with all of them, and I think buyers should understand what each one means for the market right now.

First, remove DPS for ECs entirely. If normal private condos cannot offer it, a subsidised government hybrid should not be able to either. Paying as the building goes up means you find out quickly whether you can afford it. That is the point. The BT report calls this the most direct way to bring buyer behaviour back in line with actual affordability.

Second, extend the minimum time you must live there before selling, from 5 years to 10 years. HDB Plus and Prime flats already carry a 10-year rule. If the EC is your home, not your investment, 10 years is not a burden. If you are buying to flip quickly for profit, this rule slows you down. That is exactly what it is designed to do.

Third, limit who can buy a resale EC in the years just after that rule ends. Right now anyone can buy once the EC hits the open market. That wide pool of potential buyers is part of why developers feel confident charging so much at launch. Narrow it to eligible EC buyers only, and you take some heat out of the price at source.

What to Do Before You Sign Anything

If you are looking at an EC today, do one simple check before anything else. Divide the total purchase price by your gross yearly household income. If the number is above 7, you are in risky territory. If it is above 8, you are making a speculative play, not buying a family home.

Do not choose DPS unless a bank has already given you written approval for the full loan amount. A pre-approval letter is not a loan approval. A lot can change in four years, including your job, your income, and the interest rate environment. DPS helps the developer sell units quickly. It does not protect you.

If you already own an Executive Condominium unit bought before 2021, you are sitting well. The market has moved sharply in your favour. Think clearly about how and when to use that position.

The Uncomfortable Truth About Executive Condominiums in Singapore

Every time the government raises the income ceiling so more households can “afford” an EC, it hands developers a bigger market and room to push prices higher. The subsidy meant to help buyers get in becomes the fuel that prices them out. The BT report notes the income ceiling may rise again soon, and warns this will simply give developers more reason to charge more.

The buyers hurt most by this are the ones the scheme was built to protect. Middle-income families without large savings cannot survive a DPS failure. They are not the ones making up 71 per cent of buyers using deferred terms. They are the ones outside the queue, already priced out.

The EC is no longer a stepping stone for the average Singaporean family. It has become a government-backed investment vehicle for top earners. Until the rules reward people who genuinely want a home over those chasing a five-year flip, buying an EC is not the safe bet it once was. It is a high-stakes gamble dressed up as affordable housing, and the house always wins.

About the Author

Andy Seng (RES Licence: R058286J) is a licensed real estate agent in Singapore with hands-on experience across HDB and private homes. He gives straight-talking, data-led advice to buyers, sellers, and investors in one of Asia’s most competitive property markets. When he is not at a viewing or studying URA data, he writes to help everyday Singaporeans make smarter property decisions.

This article reflects Andy’s personal views based on his professional experience. It is not financial or legal advice. Always do your own research and speak to a licensed financial adviser before making any property decision.